Tractors

Trucks

- Find by Budget

- Find by Type

Buses

- Find by Budget

- Find by Type

English

Kisan Credit Card (KCC) offers farmers affordable, flexible loans for crop cultivation, allied activities, and household needs with low interest, insurance benefits, digital access, and a simplified application process.

By CMV360 Editorial Staff

The Kisan Credit Card (KCC) scheme is one of the most significant financial initiatives taken for the welfare of Indian farmers. Launched in 1998 by NABARD and the Government of India, it was designed to provide farmers with a swift, flexible, and hassle-free credit system that caters to their various agricultural needs.

Before the KCC scheme, farmers had to depend heavily on informal credit sources such as moneylenders, often at very high interest rates. This not only increased financial pressure but also kept many farmers trapped in debt. The introduction of KCC transformed this scenario by offering a formal, affordable, and structured credit system through banks.

Over time, the scheme has evolved to meet modern farming requirements. In 2004, the KCC was expanded to include credit for investment purposes, such as dairy, poultry, fisheries, farm mechanization, and land development. Later, in 2012, the scheme underwent further simplification to introduce Electronic KCC cards, making the system more transparent and technology-friendly.

Finally, on 18 December 2020, the Prime Minister launched the Revised KCC Scheme, aimed at providing farmers easy credit under a single window for crop cultivation, allied activities, and household needs.

Agriculture in India is still highly dependent on seasonal factors, weather fluctuations, and market uncertainties. Farmers often face issues like:

The Kisan Credit Card addresses all these issues by offering:

Thus, KCC acts as a financial backbone for rural India, helping Indian farmers plan their agricultural operations efficiently.

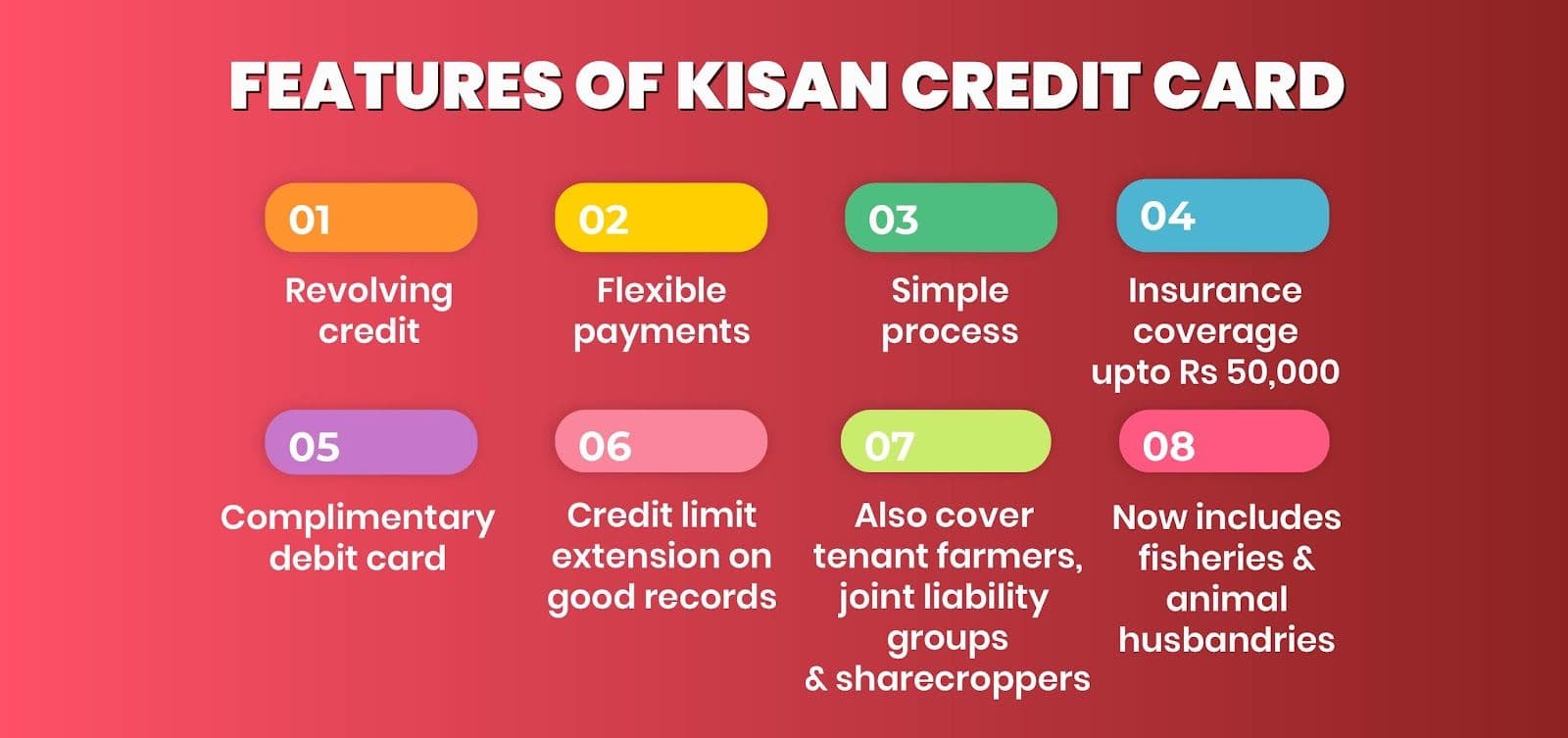

The Kisan Credit Card scheme provides a range of features and benefits to farmers including access to credit for agricultural and allied activities. This includes investment credit for requirements such as dairy animals and pump sets, as well as loans of up to Rs.3 lakh and produce marketing loans.

The scheme also provides insurance coverage for cardholders in the case of permanent disability or death, with a cover of up to Rs.50,000, and a cover of Rs.25,000 for other risks. Eligible farmers will receive a savings account with an attractive interest rate, as well as a smart card and debit card, in addition to their Kisan Credit Card.

Flexible repayment options are available, and the disbursement procedure is hassle-free. The scheme provides a single credit facility or term loan for all agricultural and ancillary requirements, and assists farmers in purchasing fertilizers, seeds, etc., and availing cash discounts from merchants and dealers.

Credit is available for a period of up to three years, with repayment made once the harvest season is over. Additionally, no collateral is required for loans amounting up to Rs.1.60 lakh. These features and benefits make the Kisan Credit Card scheme an important tool for farmers seeking to finance their agricultural activities and expand their operations.

To keep pace with digital banking, KCC cards may include:

Works at ATMs and micro-ATMs.

Useful for farmers without PIN-based literacy.

Safer, globally accepted (within India), and can be used at all merchant outlets.

Used with compatible PoS devices for secure, rural-friendly transactions.

Delivery Channels for Usage

Farmers can withdraw and transact via:

This makes KCC highly accessible even in remote rural areas.

The Kisan Credit Card loan scheme has certain eligibility criteria, which are as follows:- Any individual farmer who is an owner-cultivator is eligible.- People who belong to a group and are joint borrowers can apply. The group has to be owner-cultivators.- Sharecroppers, tenant farmers, or an oral lessee are eligible for the KCC.- Self-help groups (SHG) or joint liability groups (JLG) of sharecroppers, farmers, tenant farmers, etc. are eligible.- Farmers involved in the production of crop or allied activities such as animal husbandry along with non-farm activities such as fishermen can apply for the scheme.

The scheme for fisheries and animal husbandry has designated the following groups as eligible beneficiaries:

For Inland Fisheries and Aquaculture: Fish farmers, fishers, Self-Help Groups (SHGs), Joint Liability Groups (JLGs), and women's groups. To qualify as a beneficiary, you must either own or lease a property related to fisheries. This includes owning or leasing a pond, an open water body, a tank, or a hatchery, among others.

For Marine Fisheries: You must own a registered boat or any other type of fishing vessel, and possess the necessary license or permissions to fish in estuaries or the sea.

For Poultry: Individual farmers or joint borrowers, Self-Help Groups (SHGs), Joint Liability Groups (JLGs), and tenant farmers of sheep, rabbits, goats, pigs, birds, and poultry who own, rent or lease sheds.

For Dairy: Farmers, dairy farmers, Self-Help Groups (SHGs), Joint Liability Groups (JLGs), and tenant farmers who own, lease, or rent sheds.

To apply for the KCC Loan Scheme, the following documents are necessary:

The Kisan Credit Card application process can be completed through both online and offline methods. Here are the steps to follow:

Online:- Go to the website of the bank where you want to apply for the Kisan Credit Card scheme.- Select the Kisan Credit Card option from the list of options.- Click on the 'Apply' button, which will redirect you to the application page.- Fill in the required details on the form and click on 'Submit'.- An application reference number will be sent to you upon submission.- If you are eligible, the bank will contact you within 3-4 working days for further processing.

Offline:- You can visit the bank branch of your choice to apply for the Kisan Credit Card.- Alternatively, you can download the application form from the bank's website.- Complete the form and submit it to the bank representative.- The loan officer at the bank will help you with the loan amount once the formalities are completed.

The Indian government launched the PM Kisan Samman Nidhi Scheme, which provides income support of up to Rs. 6,000 annually to all farmers. This scheme was introduced during the 2019 Interim Union Budget of India.

After the Budget 2020, the government has taken measures to ensure that institutional credit is more accessible to all farmers in the country. To achieve this, the Kisan Credit Card (KCC) Scheme and the Kisan Samman Nidhi Scheme have been combined. As a result, all beneficiaries of the Kisan Samman Nidhi Scheme are eligible to receive a Kisan Credit Card.

The process to apply for a Kisan Credit Card under the PM Kisan Samman Nidhi Scheme is as follows:

Banks offering Kisan Credit Card (KCC) loans in India are considering longer loan repayment periods due to the significant pressure on the agriculture sector. At a state-level bankers' consultancy meeting in West Bengal, it was proposed to increase the loan repayment cycle from 12 months to 36 or 48 months.

Moreover, the banks have suggested that farmers be allowed to access additional loans even after failing to repay the previous loan, provided they service the interest. Public sector banks have initiated a three-stage consultation process based on the directions of the Department of Financial Services. The consultation process will focus on nine key issues, including credit for MSMEs and the agricultural sector, digital banking, direct transfer of benefits, and education loans. While the previous meeting was an intra-bank meet, the upcoming meeting will be an inter-bank meet at a state level.

Banks offer different Kisan Credit Cards that have various features, including credit limit and maximum tenure. Here are some of the top Kisan Credit Cards offered by different banks in India:

Axis Kisan Credit Card: The credit limit for this card is up to Rs.2.50 lakh in the form of a loan against the card. The maximum tenure for cash credit is up to 1 year, and up to 7 years for term loans.

BOI Kisan Credit Card: This card offers a credit limit of up to 25% of the farmer's estimated income, but not exceeding Rs.50,000. The maximum tenure is not applicable.

SBI Kisan Credit Card: The credit limit for this card is based on the crop cultivation and cropping pattern. The maximum tenure for this card is 5 years.

HDFC Kisan Credit Card: This card offers a credit limit of up to Rs.3 lakh, and the maximum tenure is 5 years.

To apply for a Kisan Credit Card, you can now complete the process online through any bank that issues KCCs. To check the balance of your Kisan Credit Card, you can contact the customer care of the bank that issued your card. Alternatively, you can log into the bank's website and check your Kisan Credit Card balance through their portal.

The Kisan Credit Card (KCC) scheme has become a crucial financial support system for India’s farmers. By offering easy, timely, and low-interest credit, it reduces dependence on moneylenders and helps farmers manage cultivation, household needs, and long-term investments. With features like flexible withdrawals, insurance coverage, collateral-free loans, and technology-enabled RuPay cards, KCC ensures financial security throughout the farming cycle. Its inclusive approach benefits owner cultivators, tenant farmers, sharecroppers, and SHGs alike. As the scheme continues to evolve with digital improvements, KCC remains a powerful tool that strengthens rural livelihoods and boosts India’s agricultural growth.