Tractors

Trucks

- Find by Budget

- Find by Type

Buses

- Find by Budget

- Find by Type

English

FADA CV sales August 2025 show 75,592 units sold. Mahindra records strong growth, Tata leads but loses share, Ashok Leyland and VECV improve, Switch Mobility EV sales surge.

By Robin Kumar Attri

Total CV sales stood at 75,592 units, a slight YoY rise but a marginal MoM dip.

The LCV segment grew 8.16% YoY, while the MCV saw the strongest 21.39% rise.

Tata Motors remained the market leader but lost market share to Mahindra.

Mahindra & Mahindra posted strong growth across both CV and Last Mile Mobility.

Ashok Leyland and VECV also improved sales performance year-on-year.

The Federation of Automobile Dealers Associations (FADA) has released retail sales data for commercial vehicles (CVs) in August 2025. A total of 75,592 CVs were sold, compared to 76,439 units in July 2025 and 69,635 units in August 2024.

This shows a 1.11% month-on-month (MoM) decline but an 8.55% year-on-year (YoY) growth, signaling steady demand despite monthly fluctuations.

Also Read: FADA Retail CV Sales Report July 2025: Tata Leads with Over 25,000 Units, Total Sales Reach 76,439

Category | Aug 2025 | Jul 2025 | Aug 2024 | MoM Growth | YoY Growth |

Total CV | 75,592 | 76,439 | 69,635 | -1.11% | +8.55% |

LCV | 46,156 | 45,808 | 42,672 | +0.76% | +8.16% |

MCV | 6,970 | 7,414 | 5,742 | -5.99% | +21.39% |

HCV | 22,412 | 23,154 | 21,159 | -3.20% | +5.92% |

Others | 54 | 63 | 62 | -14.29% | -12.90% |

Commercial Vehicles (CV): In August 2025, the total commercial vehicle sales stood at 75,592 units. This is lower than 76,439 units sold in July 2025 but higher than 69,635 units in August 2024. This indicates a 1.11% month-on-month (MoM) decline but a healthy 8.55% year-on-year (YoY) growth.

Light Commercial Vehicles (LCV): A total of 46,156 LCVs were sold in August 2025. This is higher than 45,808 units in July 2025 and 42,672 units in August 2024. The segment recorded a 0.76% MoM growth and an 8.16% YoY increase.

Medium Commercial Vehicles (MCV): In this segment, 6,970 units were sold in August 2025, compared to 7,414 units in July 2025 and 5,742 units in August 2024. The MCV segment showed a 5.99% MoM decline but registered a strong 21.39% YoY growth.

Heavy Commercial Vehicles (HCV): HCV sales reached 22,412 units in August 2025, down from 23,154 units in July 2025 but higher than 21,159 units in August 2024. The segment posted a 3.20% MoM decline but recorded a 5.92% YoY rise.

Others: The ‘Others’ category recorded 54 units in August 2025, lower than 63 units in July 2025 and 62 units in August 2024. This category experienced a 14.29% MoM decline and a 12.90% YoY drop.

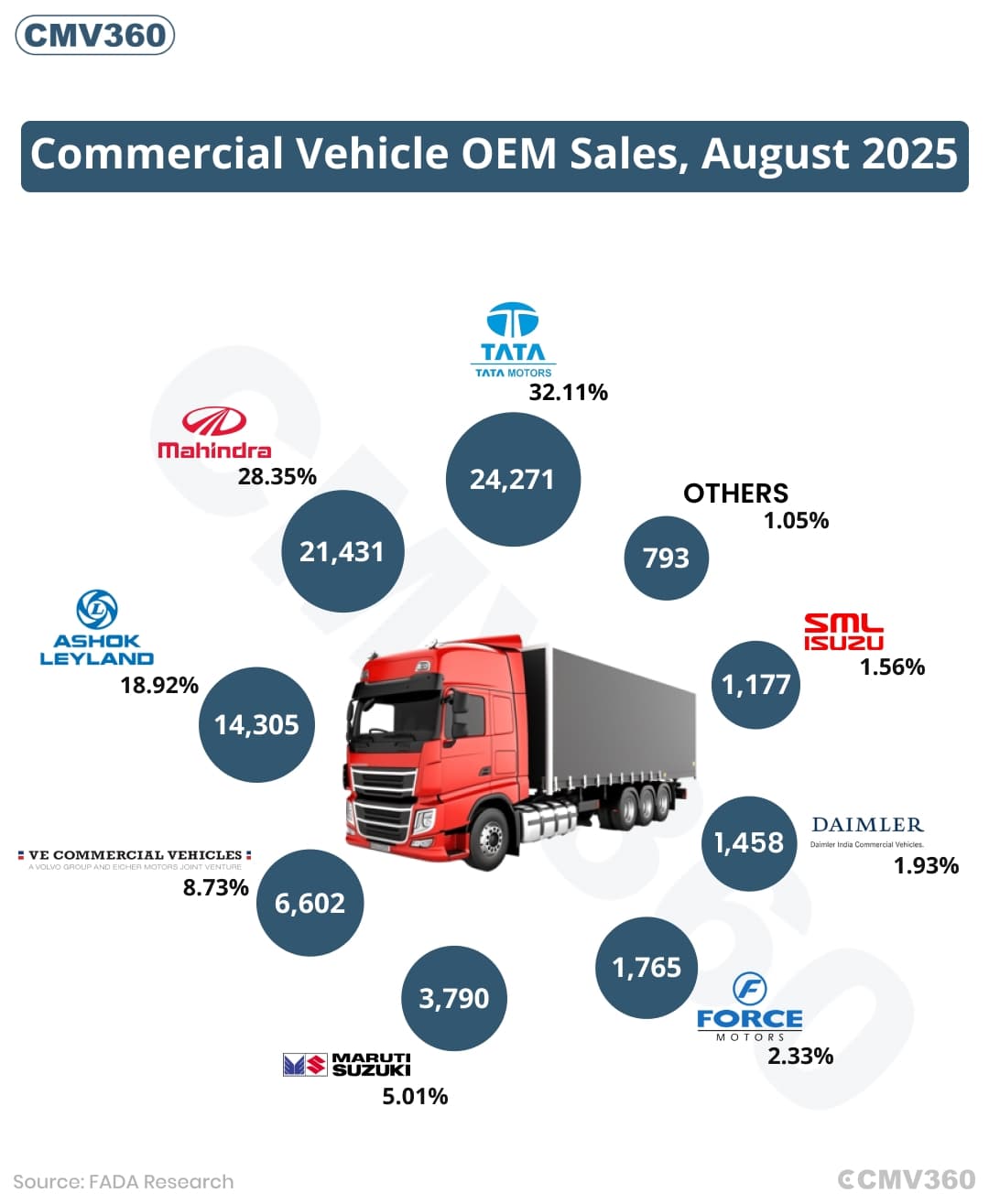

The detailed Brand OEM market share data shows key trends:

CV OEM | Aug 2025 Sales | Market Share Aug 2025 | Aug 2024 Sales | Market Share Aug 2024 |

Tata Motors Ltd | 24,271 | 32.11% | 24,928 | 35.80% |

Mahindra & Mahindra Ltd | 21,431 | 28.35% | 18,460 | 26.51% |

Mahindra & Mahindra Ltd (Second Entry) | 19,830 | 26.23% | 16,899 | 24.27% |

Mahindra Last Mile Mobility Ltd | 1,601 | 2.12% | 1,561 | 2.24% |

Ashok Leyland Ltd | 14,305 | 18.92% | 12,071 | 17.33% |

Ashok Leyland Ltd (Second Entry) | 14,032 | 18.56% | 12,038 | 17.29% |

Switch Mobility Automotive Ltd | 273 | 0.36% | 33 | 0.05% |

VE Commercial Vehicles Ltd | 6,602 | 8.73% | 6,296 | 9.04% |

VE Commercial Vehicles Ltd (Second Entry) | 6,555 | 8.67% | 6,227 | 8.94% |

VE Commercial Vehicles (Volvo Buses Division) | 47 | 0.06% | 69 | 0.10% |

Maruti Suzuki India Ltd | 3,790 | 5.01% | 3,452 | 4.96% |

Force Motors Ltd | 1,765 | 2.33% | 1,424 | 2.04% |

Daimler India CV Pvt. Ltd | 1,458 | 1.93% | 1,494 | 2.15% |

SML Isuzu Ltd | 1,177 | 1.56% | 1,018 | 1.46% |

Others | 793 | 1.05% | 492 | 0.71% |

Total | 75,592 | 100% | 69,635 | 100% |

Tata Motors retained the top spot in the CV segment by retailing 24,271 units in August 2025. However, this was slightly lower than 24,928 units sold in August 2024. Its market share declined from 35.80% to 32.11%, though the company continues to lead with a strong lineup across HCVs and LCVs.

The Mahindra Group, consisting of Mahindra & Mahindra Ltd and Mahindra Last Mile Mobility Ltd, showed solid growth in August 2025.

Mahindra & Mahindra Ltd contributed 21,431 units, rising from 18,460 units in August 2024. Its market share improved from 26.51% to 28.35%.

A second Mahindra & Mahindra listing accounted for 19,830 units, compared to 16,899 units a year ago, with market share increasing from 24.27% to 26.23%.

Mahindra Last Mile Mobility Ltd (MLMM) sold 1,601 units, slightly higher than 1,561 units last year. Its market share eased from 2.24% to 2.12%, but the company continues to show steady demand in the EV-based last-mile space.

Together, the Mahindra Group reflected robust year-on-year growth, driven by demand for both LCVs and electric commercial solutions.

The Ashok Leyland Group recorded strong numbers with sales crossing 14,300 units.

Ashok Leyland Ltdsold 14,305 units under one listing and 14,032 units under another, both higher than the 12,000+ units sold in August 2024. Its market share improved to about 18.9%, up from nearly 17.3% a year earlier.

Switch Mobility Automotive Ltd, the EV arm, saw a remarkable jump with 273 units, compared to just 33 units in August 2024. Its share increased from 0.05% to 0.36%, signaling growing adoption of electric buses and mobility solutions.

VE Commercial Vehicles maintained a steady position, selling 6,602 units compared to 6,296 units in August 2024. Its market share was at 8.73%, slightly lower than last year’s 9.04%. A second listing also reported 6,555 units, showing consistent demand in the medium CV segment.

Additionally, the Volvo Buses division of VECV recorded 47 units, down from 69 units last year, reflecting a small decline in this niche segment.

Maruti Suzuki recorded 3,790 units in August 2025, higher than 3,452 units in August 2024. Its market share improved slightly from 4.96% to 5.01%, supported mainly by the popularity of its Super Carry model.

Force Motors registered 1,765 units, growing from 1,424 units a year earlier. Its market share rose from 2.04% to 2.33%, highlighting continued demand for its passenger carriers and goods carriers.

Daimler India sold 1,458 units in August 2025, a small drop compared to 1,494 units in August 2024. Its market share declined from 2.15% to 1.93%, pointing to tough competition in the premium CV category.

SML Isuzu improved sales to 1,177 units, up from 1,018 units last year. Its market share rose from 1.46% to 1.56%, supported by demand in rural and institutional fleets.

Other manufacturers together contributed 793 units, a rise from 492 units in August 2024. Their combined market share improved from 0.71% to 1.05%, showing growing traction among smaller and niche CV brands.

Also Read: FADA Three-Wheeler Retail Sales Report August 2025: Over 1.03 Lakh Units Sold

The August 2025 FADA CV retail data shows a mixed performance. While total sales dipped slightly month-on-month, the strong year-on-year growth signals robust demand recovery. Mahindra’s sharp growth and Switch Mobility’s surge in EV sales are key highlights, while Tata Motors faces pressure with declining market share.

Segment-wise, LCV and MCV remain the biggest growth drivers, while HCV demand is steady but slightly under pressure. With electrification and light CV demand rising, the Indian CV industry is expected to maintain positive momentum going ahead.