Tractors

Trucks

- Find by Budget

- Find by Type

Buses

- Find by Budget

- Find by Type

English

FADA July 2025 CV sales report shows steady growth, with Tata leading and Mahindra gaining strong market share momentum.

By Robin Kumar Attri

Total CV sales stood at 76,439 units, a small YoY rise and good MoM improvement.

LCV and MCV segments posted positive growth, with MCV rising over 10% YoY.

Tata Motors led the market but saw a decline in volume and share.

Mahindra & Mahindra showed strong momentum and improved market position.

Switch Mobility and SML Isuzu reported notable YoY growth.

The Federation of Automobile Dealers Associations (FADA) has released the retail sales data for Commercial Vehicles (CVs) for July 2025. The industry showed a marginal year-on-year growth, with a total of 76,439 units sold, compared to 76,261 units in July 2024, a slight increase of 0.23%. Month-on-month, the segment registered a healthy 4.19% growth compared to 73,367 units sold in June 2025.

Category | July 2025 | June 2025 | July 2024 | MoM Growth | YoY Growth |

Total CV | 76,439 | 73,367 | 76,261 | +4.19% | +0.23% |

LCV | 45,808 | 44,469 | 45,565 | +3.01% | +0.53% |

MCV | 7,414 | 7,393 | 6,712 | +0.28% | +10.46% |

HCV | 23,154 | 21,447 | 23,912 | +7.96% | -3.17% |

Others | 63 | 58 | 72 | +8.62% | -12.50% |

Commercial Vehicles: In July 2025, the total commercial vehicle (CV) sales stood at 76,439 units. This is higher than 73,367 units sold in June 2025 and 76,261 units in July 2024. This indicates a 4.19% month-on-month (MoM) growth and a marginal 0.23% year-on-year (YoY) increase.

Light Commercial Vehicles (LCV): A total of 45,808 LCVs were sold in July 2025. This is an increase from 44,469 units in June 2025 and 45,565 units in July 2024. The segment recorded a 3.01% MoM growth and a slight 0.53% YoY rise.

Medium Commercial Vehicles (MCV): In this segment, 7,414 units were sold in July 2025, compared to 7,393 units in June 2025 and 6,712 units in July 2024. The MCV segment showed a 0.28% MoM increase and a strong 10.46% YoY growth.

Heavy Commercial Vehicles (HCV): HCV sales reached 23,154 units in July 2025, up from 21,447 units in June 2025 but down from 23,912 units in July 2024. The segment posted a healthy 7.96% MoM rise but saw a 3.17% YoY decline.

Others: The ‘Others’ category recorded 63 units in July 2025, up from 58 units in June 2025 but down from 72 units in July 2024. This category experienced an 8.62% MoM growth but a 12.50% YoY decline.

The table below shows how various commercial vehicle manufacturers performed in July 2025 compared to July 2024:

OEM | July 2025 Sales | Market Share (%) July 2025 | July 2024 Sales | Market Share (%) July 2024 |

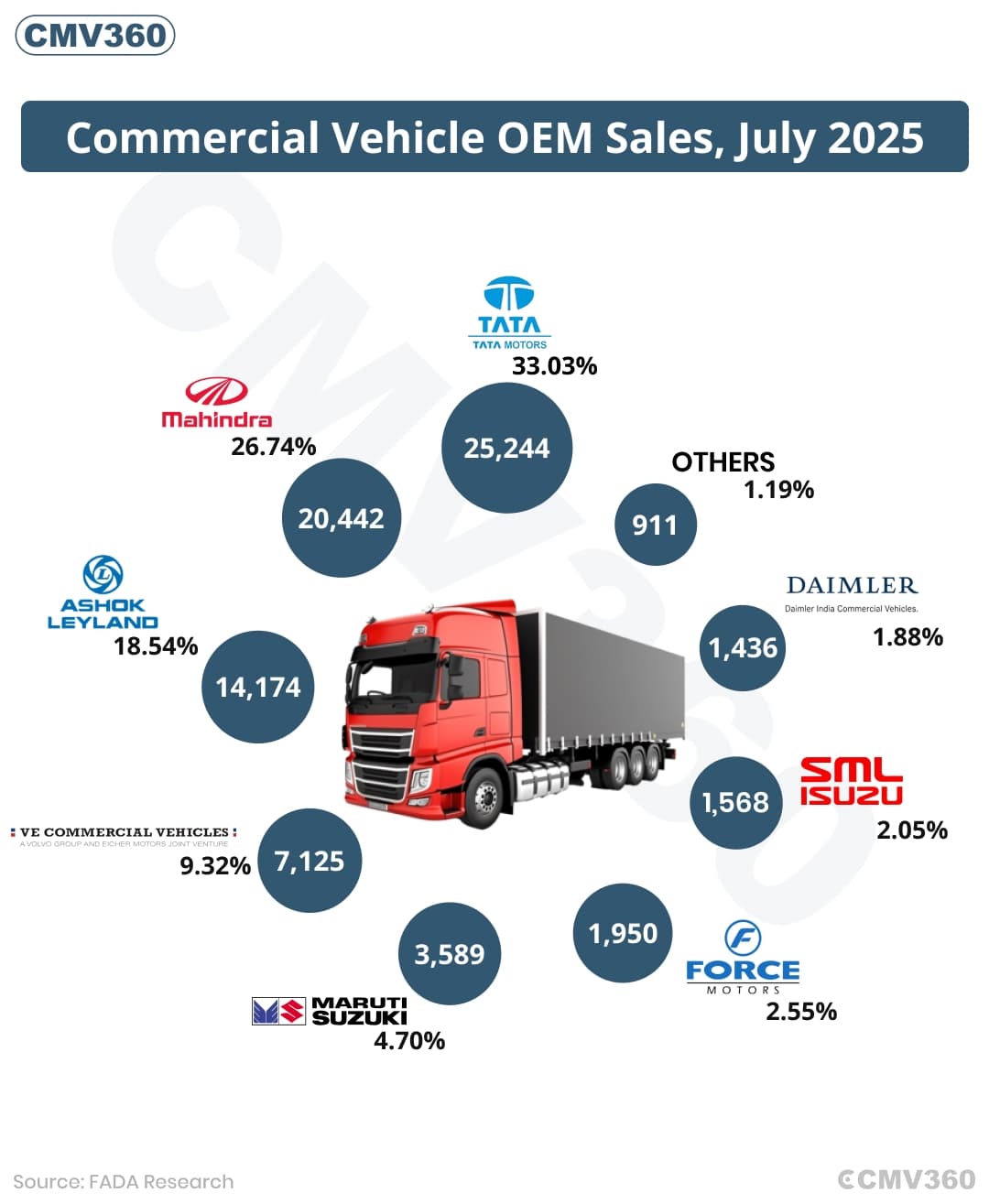

Tata Motors Ltd | 25,244 | 33.03% | 27,617 | 36.21% |

Mahindra & Mahindra Ltd | 20,442 | 26.74% | 19,039 | 24.97% |

MAHINDRA & MAHINDRA LIMITED | 18,950 | 24.79% | 17,578 | 23.05% |

Mahindra Last Mile Mobility Ltd | 1,492 | 1.95% | 1,461 | 1.92% |

Ashok Leyland Ltd | 14,174 | 18.54% | 13,979 | 18.33% |

ASHOK LEYLAND LTD | 14,078 | 18.42% | 13,940 | 18.28% |

Switch Mobility Automotive Ltd | 96 | 0.13% | 39 | 0.05% |

VE Commercial Vehicles Ltd | 7,125 | 9.32% | 6,689 | 8.77% |

Maruti Suzuki India Ltd | 3,589 | 4.70% | 3,543 | 4.65% |

Force Motors Ltd | 1,950 | 2.55% | 1,901 | 2.49% |

SML Isuzu Ltd | 1,568 | 2.05% | 1,431 | 1.88% |

Daimler India CV Pvt. Ltd | 1,436 | 1.88% | 1,581 | 2.07% |

Others | 911 | 1.19% | 481 | 0.63% |

Total | 76,439 | 100.00% | 76,261 | 100.00% |

Tata Motors retained the top spot in the CV segment by retailing 25,244 units in July 2025. However, this was a decline from 27,617 units in July 2024. Its market share fell from 36.21% to 33.03%, though the company still leads with a strong portfolio across HCVs and LCVs.

The Mahindra Group, including Mahindra & Mahindra Ltd and Mahindra Last Mile Mobility Ltd, registered a combined retail of 20,442 units in July 2025, up from 19,039 units in July 2024. This reflects a market share increase from 24.97% to 26.74% showing the growing demand across its LCV range and last-mile commercial offerings.

Within this, Mahindra & Mahindra Ltd contributed 18,950 units (up from 17,578 units), accounting for 24.79% market share, while Mahindra Last Mile Mobility Ltd sold 1,492 units (up from 1,461 units), holding a steady 1.95% market share. The group showed strong year-on-year growth, driven by continued demand in both LCV and last-mile electric vehicle segments.

The Ashok Leyland Group, comprising Ashok Leyland Ltd and Switch Mobility Automotive Ltd, recorded total retail sales of 14,174 units in July 2025, a rise from 13,979 units in July 2024. This took the group’s combined market share to 18.54%, up from 18.33% last year.

Out of this, Ashok Leyland Ltd contributed 14,078 units, slightly higher than 13,940 units sold last year, maintaining a market share of 18.42%.

Meanwhile, its electric vehicle arm, Switch Mobility, saw a significant jump with 96 units sold in July 2025, up from just 39 units in July 2024, increasing its market share from 0.05% to 0.13% — indicating rising interest in electric commercial vehicles.

VE Commercial Vehicles grew steadily with 7,125 units sold, up from 6,689 units in July 2024. Its market share improved from 8.77% to 9.32%, showing a strong presence in mid-size commercial vehicles.

Maruti Suzuki’s CV sales touched 3,589 units, up slightly from 3,543 units last year. Its market share rose marginally to 4.70%, with continued interest in its Super Carry model.

Force Motors delivered a stable performance with 1,950 units sold, improving from 1,901 units in July 2024. Its market share grew slightly to 2.55%, reflecting steady demand for its passenger and goods carriers.

SML Isuzu increased its CV retail to 1,568 units, up from 1,431 units in July last year. Its share rose from 1.88% to 2.05%, supported by strong rural and institutional demand.

Daimler India saw a slight dip, selling 1,436 units in July 2025 compared to 1,581 units last year. Its market share declined from 2.07% to 1.88%, possibly due to stiff competition in the premium CV space.

All other brands combined contributed 911 units, up from 481 units last year. Their collective market share rose from 0.63% to 1.19%, showcasing growing interest in new or niche commercial vehicle players.

Also Read: FADA Sales Report June 2025: CV sales increased by 6.60% YoY

The July 2025 FADA retail data reveals a steady market with signs of recovery and expansion in specific segments. While giants like Tata Motors maintain leadership, rising brands like Mahindra, Ashok Leyland, and VECV continue to gain ground. The jump in MCV sales and increased share of alternative mobility brands like Switch Mobility indicate a shift in buyer preferences toward newer formats and electrification.

However, the slight dip in HCV sales and Tata’s market share drop point to challenges in freight and infrastructure-dependent segments. Overall, the outlook for the CV industry remains cautiously optimistic with positive signs in retail demand.