Tractors

Trucks

- Find by Budget

- Find by Type

Buses

- Find by Budget

- Find by Type

English

FADA December 2025 CV sales hit 83,666 units. Tata Motors led the market as LCVs dominated volumes, and infrastructure-driven demand kept the commercial vehicle market stable.

By Robin Kumar Attri

Total CV retail sales stood at 83,666 units in December 2025.

The LCV segment remained the highest contributor despite a YoY decline.

The MCV segment recorded the strongest growth over the earlier period.

Tata Motors led the market with over 35% share.

Electric and niche OEMs showed gradual volume improvement.

India’s commercial vehicle (CV) retail market recorded 83,666 units in December 2025, according to FADA Research. While overall sales showed a 9.65% year-on-year decline, demand remained steady across key segments, supported by logistics movement, fleet replacement, and infrastructure activity.

Total CV retail sales stood at 83,666 units, compared to 92,604 units in December 2024 and 67,145 units earlier, indicating mixed market sentiment with pressure on year-on-year growth but stability in core demand.

Category | Retail Sales Dec’25 (Units) | Retail Sales Dec’24 (Units) | Retail Sales (Earlier Period) | YoY Change vs Dec’24 | Change vs Earlier Period |

Total CV | 83,666 | 92,604 | 67,145 | -9.65% | +24.60% |

LCV | 49,251 | 56,637 | 40,222 | -13.04% | +22.45% |

MCV | 6,411 | 7,234 | 4,215 | -11.38% | +52.10% |

HCV | 27,941 | 28,659 | 22,637 | -2.51% | +23.43% |

Others | 63 | 74 | 71 | -14.86% | -11.27% |

The LCV segment remained the largest contributor with 49,251 units sold. However, sales declined 13.04% YoY, reflecting cautious buying in last-mile and small fleet operations. Despite this, the segment posted 22.45% growth over the previous base period, showing underlying demand strength.

MCV sales reached 6,411 units, down 11.38% YoY. Compared to earlier volumes, the segment registered a strong 52.10% growth, supported by industrial and institutional usage.

HCVs recorded 27,941 units, marking a marginal 2.51% decline YoY. The segment still showed 23.43% growth over the earlier period, driven by freight, mining, and infrastructure projects.

The “Others” category stood at 63 units, showing a 14.86% YoY decline and a 11.27% drop over the base period, as niche and low-volume OEMs faced demand pressure.

OEM / Brand | Retail Sales (Units) | Market Share Dec’25 | Retail Sales Dec’24 | Market Share Dec’24 |

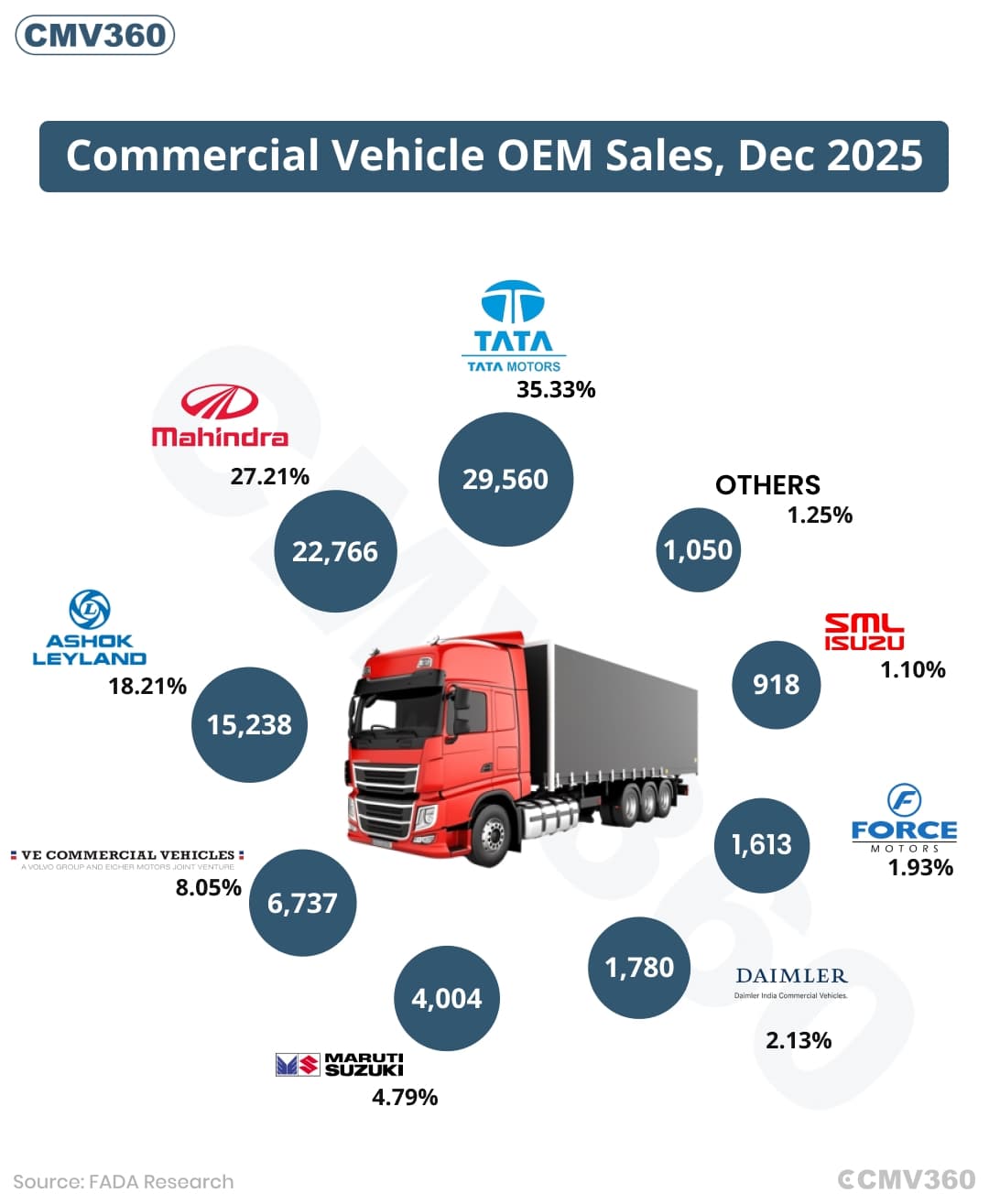

Tata Motors Ltd | 29,560 | 35.33% | 24,327 | 36.23% |

Mahindra & Mahindra Ltd | 22,766 | 27.21% | 18,917 | 28.17% |

Mahindra & Mahindra Ltd (2nd Entry) | 21,504 | 25.70% | 17,516 | 26.09% |

Mahindra Last Mile Mobility Ltd | 1,262 | 1.51% | 1,401 | 2.09% |

Ashok Leyland Ltd | 15,238 | 18.21% | 11,745 | 17.49% |

Ashok Leyland Ltd (2nd Entry) | 14,918 | 17.83% | 11,648 | 17.35% |

Switch Mobility Automotive Ltd | 320 | 0.38% | 97 | 0.14% |

VE Commercial Vehicles Ltd | 6,737 | 8.05% | 4,594 | 6.84% |

VE Commercial Vehicles Ltd (2nd Entry) | 6,656 | 7.96% | 4,529 | 6.75% |

VE Commercial Vehicles Ltd (Volvo Buses Division) | 81 | 0.10% | 65 | 0.10% |

Maruti Suzuki India Ltd | 4,004 | 4.79% | 3,550 | 5.29% |

Force Motors Ltd | 1,613 | 1.93% | 1,280 | 1.91% |

Daimler India Commercial Vehicles Pvt. Ltd | 1,780 | 2.13% | 1,600 | 2.38% |

SML Isuzu Ltd | 918 | 1.10% | 644 | 0.96% |

Others | 1,050 | 1.25% | 488 | 0.73% |

Total | 83,666 | 100.00% | 67,145 | 100.00% |

Tata Motors emerged as the market leader in December 2025 with retail sales of 29,560 units, capturing a 35.33% market share. Although slightly lower than 36.23% in December 2024, the company maintained its top position due to strong demand across both light and heavy commercial vehicle segments and its wide nationwide dealership network.

Mahindra & Mahindra reported 22,766 units in December 2025, securing a 27.21% market share, compared to 28.17% last year. The brand continued to perform well in pickups and small commercial vehicles, supported by steady rural and fleet demand.

Mahindra & Mahindra Ltd (Second Entry): Under its second reporting entry, Mahindra & Mahindra sold 21,504 units, accounting for a 25.70% market share, slightly lower than 26.09% in December 2024. This reflects consistent demand across multiple CV sub-segments within Mahindra’s portfolio.

Mahindra Last Mile Mobility Ltd: Mahindra Last Mile Mobility recorded 1,262 units, with its market share declining to 1.51% from 2.09% last year. The softer performance indicates moderated demand in the last-mile mobility and electric small commercial vehicle space.

Ashok Leyland posted retail sales of 15,238 units, achieving an 18.21% market share, up from 17.49% in December 2024. The company benefited from steady demand in medium and heavy trucks, along with bus segment orders.

Ashok Leyland Ltd (Second Entry): In its second entry, Ashok Leyland recorded 14,918 units with a 17.83% market share, compared to 17.35% last year, reflecting stable growth across institutional and fleet-based sales.

Switch Mobility Automotive Ltd: Switch Mobility sold 320 units in December 2025, holding a 0.38% market share, up from 0.14% in December 2024. The improvement highlights rising adoption of electric buses, particularly in urban public transport projects.

VE Commercial Vehicles reported 6,737 units, capturing an 8.05% market share, compared to 6.84% last year. The brand continued to strengthen its position through its Eicher truck and Eicher bus portfolio.

VE Commercial Vehicles Ltd (Second Entry): Under its second entry, VECV sold 6,656 units, accounting for a 7.96% market share, up from 6.75% in December 2024, indicating stable and balanced growth across vehicle categories.

VE Commercial Vehicles Ltd (Volvo Buses Division): The Volvo Buses division of VECV retailed 81 units, maintaining a 0.10% market share, unchanged from last year, reflecting its niche presence in the premium bus segment.

Maruti Suzuki recorded 4,004 units in December 2025, with a 4.79% market share, slightly lower than 5.29% in December 2024. Demand remained steady for its Super Carry model in the small commercial vehicle category.

Force Motors sold 1,613 units, achieving a 1.93% market share, marginally higher than 1.91% last year. The growth was supported by demand for passenger carriers and utility vehicles.

Daimler India Commercial Vehicles reported 1,780 units, holding a 2.13% market share, down from 2.38% in December 2024, as competitive pricing and cautious fleet purchases impacted volumes.

SML Isuzu recorded 918 units in December 2025, with a 1.10% market share, improving slightly from 0.96% last year, supported by steady demand in the light and intermediate truck segments.

Other manufacturers together accounted for 1,050 units, translating to a 1.25% market share, up from 0.73% in December 2024, reflecting the gradual expansion of niche and regional commercial vehicle players.

Retail CV sales in December 2025 indicate a cautious but stable market. While year-on-year numbers declined, growth over earlier periods highlights ongoing demand from logistics, infrastructure, and freight movement. Tata Motors and Mahindra continue to dominate, while electric and alternative mobility players are gradually expanding their footprint. With infrastructure spending and fleet upgrades expected to continue, the CV market outlook remains steady heading into 2026.

Also Read: Aptiv Secures First ADAS Contract for Indian Commercial Vehicles Ahead of 2027 Safety Norms

India’s commercial vehicle retail market closed December 2025 with 83,666 units, reflecting short-term pressure but stable long-term demand. LCVs continued to dominate volumes, while MCV and HCV segments showed strong growth over earlier periods. Tata Motors retained clear leadership, followed by Mahindra and Ashok Leyland. Rising infrastructure activity, freight movement, and gradual adoption of electric mobility are expected to support a steady market outlook moving into 2026.

")